Meta Stock Is a Buy Because the Company Is Doing More With Less

[ad_1]

Cost-cutting is typically celebrated by a company’s shareholders. After all, spending less money — in theory, anyway — allows more revenue to be turned into profit.

In the real world, though, culling costs isn’t always so simple. Sometimes spending less on things like marketing, research and development, and even employees can unexpectedly undermine a company’s ability to continue doing business as usual.

Facebook parent Meta Platforms (META 2.91%) is successfully walking this fine line. During its third quarter of the year, expenses continued to dwindle, yet sales continued to grow. Indeed, the company’s top-line growth actually accelerated.

Shares fell anyway following the release of its Q3 results. However, that dip is ultimately a buying opportunity for interested investors who believe the global economy is getting better rather than getting worse. And now there’s a very good reason to think it’s getting better.

More revenue + less spending = more profit

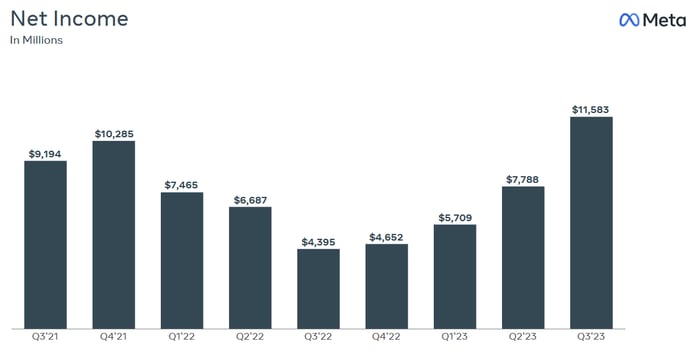

For the three-month stretch ending in September, Meta turned $34.1 billion worth of revenue into operating income of $13.7 billion and net income of $11.6 billion. Sales were up 23% year over year, but because costs and expenses were down to the tune of 7%, operating income soared 143%. Net income jumped 164% year over year. On a per-share basis, profits grew from $1.64 then to $4.39 now.

What the heck happened? It’s worth noting that a sizable chunk of Meta’s sales growth came from Chinese companies finally feeling some relief from that nation’s economic lethargy. Mostly, though, Meta just spent less money while selling more ad space to advertisers outside of China.

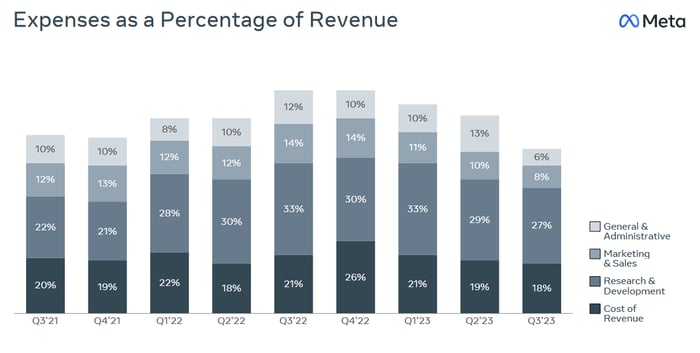

This slide from the company’s earnings presentation puts things in perspective. During the same quarter a year ago, a total of 80% of its revenue was consumed by spending on basic costs like administration, marketing, and research and development; marketing costs were up 50% year over year that quarter alone. Since the fourth quarter of last year, however, Meta’s made a point of dialing back these costs.

Image source: Meta Platforms Q3 2023 earnings call slide deck.

End result? An explosion in net income.

Image source: Meta Platforms Q3 2023 earnings call slide deck.

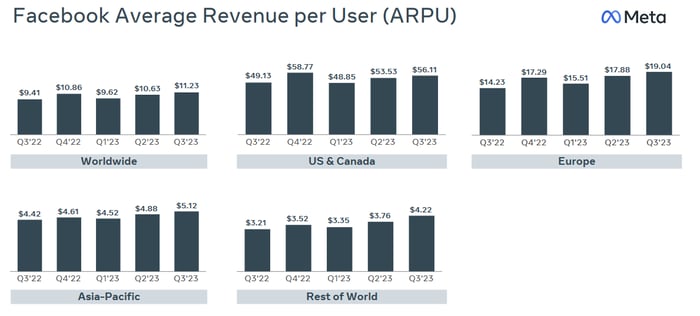

And it’s important to note that profits aren’t up solely because spending is down. Costs only fell $1.7 billion year over year, while Meta’s top line grew $6.4 billion year over year in Q3. Meta isn’t simply attracting new (or reattracting previous) users that cost more than they’re worth, either. At the same time the company’s active user base grew, its overall average revenue per user is markedly better than year-ago comparisons. That’s particularly true for its flagship platform Facebook, which now boasts a record-breaking 3.049 billion monthly users. That’s up from 2.958 billion at this point of 2022.

Image source: Meta Platforms Q3 2023 earnings call slide deck.

Connect the dots. Meta doesn’t have to spend a ton of money — particularly on marketing — to draw a crowd of users or serve advertisers. It can do more with less. Indeed, it is doing more with less.

So why is the market souring on the stock following the release of its third-quarter numbers? Let’s just say the company’s trying to temper investors’ lofty expectations.

‘Softer ad spend’

While management’s mood during the company’s Q3 earnings call was anything but dour, Meta’s chiefs were clearly trying to keep investors’ expectations at realistic levels. It was one comment from CFO Susan Li, however, that arguably accounts for the bulk of Meta stock’s post-earnings tumble. She explained: “We are very subject to volatility in the macro landscape … The revenue outlook is uncertain.”

Yikes. The words in and of themselves are concerning. The fact that Li made a decision to say them when she didn’t have to, however, is outright alarming.

For good measure, Li added: “While we don’t have material direct revenue exposure to Israel and the Middle East, we have observed softer ad spend in the beginning of the fourth quarter, correlating with the start of the conflict, which is captured in our Q4 revenue outlook.”

That outlook is for a fourth-quarter top line of between $36.5 billion and $40 billion — up from the year-ago comparison of $32.2 billion, but not exactly leaps and bounds above analysts’ consensus of $36.6 billion for the quarter now underway.

Yet, there’s good reason to think advertising demand is and will be stronger than Meta’s CFO suggests.

Take the United States’ Q3 gross domestic product (GDP) growth rate as an example. It raced 4.9% higher versus expectations of only 4.7%, accelerating from Q2’s lethargic pace of 2.1%. Even stripping out the benefit of inventory growth and limiting the measure to consumer spending, last quarter’s GDP reached a healthy clip of 3.6%. In this same vein, the Census Bureau reports September’s retail spending in the U.S. was up 3.8% year over year. Meanwhile, the nation’s unemployment rate remains below 4%.

In that Facebook’s user base and ad business is almost entirely consumer-oriented, this degree of willingness to spend bodes well for the company’s U.S. market.

Things are humming again elsewhere too. While Europe’s economy continues to face a headwind, China’s National Bureau of Statistics reports its GDP improved 4.9% year over year during Q3 2023. While Facebook and Meta’s other social media platforms like Instagram and WhatsApp are banned in China, the company still benefits indirectly from the country’s economic strength.

Despite this measurable strength, many economists still doubt a so-called “soft landing” scenario — where the global economy eases back into growth mode without actually suffering a full-blown recession — is possible.

Just take these doubts with a big grain of salt. Economic forecasters don’t boast a great track record, particularly of late. This crowd’s been calling for a cyclical recession since 2019. It has not happened yet. That’s because the global economy and the stock market both have a funny way of being able to climb a wall of worry when doing so seems impossible.

Buy Meta stock here

Don’t misread the message. There’s never a bad reason to exercise a bit of healthy caution. Perhaps the slowdown in ad spending Meta’s CFO pointed out is an omen of something bigger brewing in the background. Never say never.

Also look at what Meta is doing as part of its well-defined “year of efficiency” plan put in place nearly a year ago. It’s working. These cost cuts aren’t doing more harm than good.

Yes, the company is planning capital expenditures of between $30 billion and $35 billion for 2024, up from this year’s likely range of between $27 billion and $29 billion. All told, Meta believes it will shell out somewhere between $94 billion and $99 billion next year to cover all of its costs. That’s a lot of money.

It’s seemingly unlikely these outlays will be done as indiscriminately as they were last year, however. If nothing else, CEO Mark Zuckerberg doesn’t want to face the headaches and criticisms that come with such aggressive spending that isn’t immediately paired with revenue and/or profit growth.

The market’s not seeing it from this perspective right now. It should start seeing things from this angle soon, though. And, now down 13% from their October high thanks to Thursday’s post-earnings stumble, shares are primed for a decent bounce once investors begin recognizing just how well Meta is doing.

Don’t overthink this one.

[ad_2]