This Magnificent Growth Stock Is Crushing the Market, and You May Regret Not Buying It Hand Over Fist Right Now

[ad_1]

Shares of Zscaler (ZS -0.12%) have crushed the broader technology sector this year with an impressive gain of 77%, significantly higher than the Nasdaq Composite‘s 36% rise, and it looks like this cybersecurity specialist could be heading higher after its latest earnings report.

Zscaler released fiscal 2024 first-quarter results (ended Oct. 31) on Nov. 27. The company’s revenue and earnings were well ahead of what Wall Street was anticipating. What’s more, its guidance was also better than the consensus estimates. Still, Zscaler stock remained almost flat following the earnings report as it didn’t raise its full-year billings guidance. Management adopted a conservative approach on account of potentially cautious spending from customers.

However, the absence of a post-earnings spike in Zscaler stock could be an opportunity for savvy investors to buy more shares of this cybersecurity company before it gets more expensive. Let’s look at the reasons why.

Zscaler continues to grow at an impressive pace

Zscaler’s fiscal Q1 revenue jumped 40% year over year to $497 million. The company’s non-GAAP (adjusted) net income increased at a much faster pace of 131% over the year-ago quarter to $0.67 per share. Analysts were expecting $0.49 per share in earnings on revenue of $473 million, but the healthy growth in spending from existing customers allowed the company to cruise past those estimates.

Zscaler witnessed a 22% year-over-year increase in the number of customers who have generated over $100,000 in annual recurring revenue (ARR) for the company. Meanwhile, the number of customers with an ARR of more than $1 million jumped 34%. These high-value customers are adopting multiple cybersecurity services that the company offers. CEO Jay Chaudhry remarked on the latest earnings conference call:

We also achieved a record for new pipeline generation in a quarter. More customers are adopting our broader platform to consolidate multiple-point products, increasing our average deal size. As a result, we are actively working on more large, multiyear, multi-pillar opportunities than ever before.

All this explains why Zscaler finished the quarter with a dollar-based net retention rate of 120%. This metric compares the spending of a company’s customers during the trailing-12-month period to the spending by the same customer cohort in the year-ago period. So, a reading of more than 100% suggests the company’s existing customer base is purchasing more of its offerings or expanding the use of current solutions.

The strength of these recent results led the company to raise its full-year revenue and earnings guidance. It now expects fiscal 2024 revenue to increase between 29% and 30% year over year to a range of $2.09 billion to $2.10 billion. Zscaler has also increased its earnings per share guidance to a range of $2.45 to $2.48, thanks to a jump of 250 basis points in its operating margin.

However, the company maintained the full-year billings guidance in the range of $2.52 billion to $2.56 billion, which would be an increase of 24% to 26% over fiscal 2023. That outlook fell slightly short of the $2.55 billion consensus estimate at the midpoint, but investors would do well to focus on the bigger picture as Zscaler is on track to grow nicely in fiscal 2024 despite anticipating cautious spending from customers.

CFO Remo Canessa points out that “the global macro environment remains challenging and customers continue to scrutinize large deals.” But he went on to add that Zscaler is witnessing stability in customer sentiment. Canessa also added that the company has a “large and growing pipeline,” which is evident from the 39% growth in deferred revenue last quarter to $1.4 billion.

That nearly matched the company’s actual revenue growth, and it suggests Zscaler is on track to achieve its full-year revenue target, as this metric refers to money collected by a company for services that will be rendered at a future date.

Why investors should buy the stock right now

Zscaler operates in the fast-growing cloud cybersecurity market, which is estimated to clock a compound annual growth rate of 26% through 2030 and generate almost $85 billion in revenue at the end of the forecast period, according to Verified Market Research. The firm estimates this market generated almost $11 billion in revenue in 2021, which means Zscaler could be at the beginning of a solid growth curve considering the secular opportunity it can tap into long term.

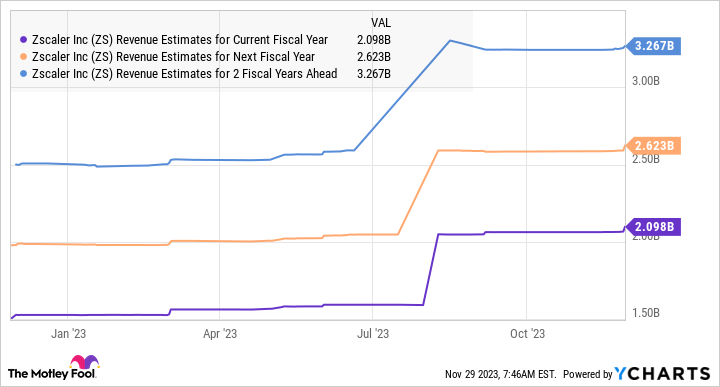

Not surprisingly, analysts are expecting the company to deliver consistently robust top-line growth over the next three years.

Data by YCharts.

They also expect 36% annual earnings growth over the next five years. As such, now would be a good time for investors to buy this growth stock, considering the relatively cheaper multiples it’s trading at as of this writing. Zscaler has a price-to-sales ratio of 16 and forward earnings multiple of 67. That’s a premium to the broad market, but those readings are lower than its five-year averages of 30 and 149, respectively.

Assuming Zscaler does hit the $3.27 billion revenue estimate in fiscal 2026 and trades at a discounted sales multiple of 15 at that time, which would be half the five-year average sales multiple, its market cap could jump to $49 billion within the next three years. That would be a 72% increase from current levels, which is why investors would do well to buy this stock before it soars higher.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Zscaler. The Motley Fool has a disclosure policy.

[ad_2]